On June 1, 2013, the National Bank of Hungary launched the Loans for Growth Program (NHP), albeit the details of the program had been known several months earlier. For the July 2013 SME Outlook survey by the HCCI Institute for Economic and Enterprise Research (IEER) the leaders of small and medium-sized enterprises were asked about bank loans and the NHP Program.

The results show that a little more than half of small and medium-sized enterprises have some form of bank loan. The most common type of credit is working capital loans (including account loans) and companies hold mostly forint-denominated loans.

During the first half of 2013, barely one third of SMEs intended to take out a loan. Most companies considered a working capital loan (account loan) while two-thirds of the firms planning to borrow took into account the NHP when making the decision. In the end, three-quarters of those planning to borrow made a loan application, of which the vast majority occurred within the NHP.

Read more >>>Within the framework of the SME Outlook research, since January 2005 the HCCI Institute for Economic and Enterprise Research (IEER) conducts a quarterly analysis of the situation of small and medium sized enterprises, their short-term prospects, as well as the economic and institutional factors affecting this business group. For this project a total of 300 companies operating within the fields of manufacturing, construction and services is surveyed and the data is analyzed in every quarter. The structure of the sample remains the same from quarter to quarter, with the companies surveyed representing the economic performance and sector distribution of small and medium sized enterprises in Hungary.

Indicators pertaining to the current situation of small and medium sized enterprises were mixed and somewhat negative for the second quarter of 2013. Compared to the previous quarter, only the business situation indicator increased for all current situation indicators. By contrast, future expectations indicate optimism, because apart from stagnation in employment numbers, all other forward-looking indicators increased; this was particularly evident in the sharp increase in anticipated investment activity.

Read more >>>

The objective of the latest of research of IEER was to get survey-based information on the intentions of high school students for higher education and how these intentions change by various high school and student traits. The survey was carried out by a brief self-administered questionnaire at a sample of secondary schools selected on the basis of several criteria. Nevertheless the sample design could not be proportional by some important features (e.g., high schools' ranking by admission rates, geographic location, or student composition). During the selection process high schools were classified into two groups based on admission rates - elite and non-elite high schools - and in addition to high schools from Budapest, several from rural areas were included as well. On the following link an English summary of the paper can be downloaded.

Read more >>>The objective of the latest research of IEER was to get survey-based information on the intentions of high school students for higher education and how these intentions change by various high school and student traits. The survey was carried out by a brief self-administered questionnaire at a sample of secondary schools selected on the basis of several criteria. Nevertheless the sample design could not be proportional by some important features (e.g., high schools' ranking by admission rates, geographic location, or student composition). During the selection process high schools were classified into two groups based on admission rates - elite and non-elite high schools - and in addition to high schools from Budapest, several from rural areas were included as well.

The study took place from 23 April to 26 June 2013, using a quota method on the basis of high school rankings. Students from six selected Budapest and rural institutions completed a questionnaire on paper or online - answering questions by computer or smart phone. Our results are based on the responses of 592 high school students.

Read more >>>In 2012 wage regulation changed in a number of ways. The changes affected 74 percent of workers; these changes, however, differed significantly depending on sector. Eighty percent of companies with between 5 and 50 employees implemented the expected wage increases. Of these, 93 percent compensated all their employees - in other words, all those affected by changes in the regulatory environment. The IEER's latest analysis examines how the increased burden due to the changes in the regulatory environment affected the employment situation of small businesses. According to the analysis, jobs would have been lost and the employment rate would have declined if the expected wage increases were compulsory and not linked to salary compensation. Due to the nature of the expected wage increase (non-compulsory) and the institution of wage compensation, however, this did not happen; at the same time, although the expected wage increases, which were partially neutralized by the institution of wage compensation, did not lead to job losses, it did make it more difficult to create new jobs.

Read more >>>

According to preliminary statistics data released by the Central Statistics Office (CSO, or KSH in Hungarian), seasonally and calendar-adjusted gross domestic product fell by 0.3% in the first quarter of 2013 compared to the same period last year, but compared to the previous quarter a 0.7% increase was observed.

Indicators pertaining to the current situation of small and medium-sized enterprises (SMEs) showed a consistent picture for the first quarter of 2013. Compared to the previous quarter, current situation indicators had all increased slightly. Expectations for the next year don't reflect this optimism, however; particularly evident is the sharp decline in expected investment activity.

The overall effect of these contradictory results has led the SME Business Climate Index to idle after experiencing a strong rise during the previous survey; although the value is still rising, it's at a much slower rate than in the previous quarter. The Uncertainty Index declined somewhat; in other words, a decline can be seen in the diversity of opinions of SME assessments toward their current and expected business situations.

The share of small and medium-sized enterprises with bank loans has been steadily declining since October 2011; its current value is at 62%. In terms of loan type, it can be stated that firms are still mostly indebted in HUF. The proportion of business loans in Euros and Swiss francs has declined significantly since April 2012, and currently represents 25% and 1.1% respectively of all SME loans.

During the past half year 17% of the businesses surveyed inquired at a bank about the possibility of borrowing money, which is a rate two percentage points lower than in April 2012.

On the following link an English summary of the paper can be downloaded.

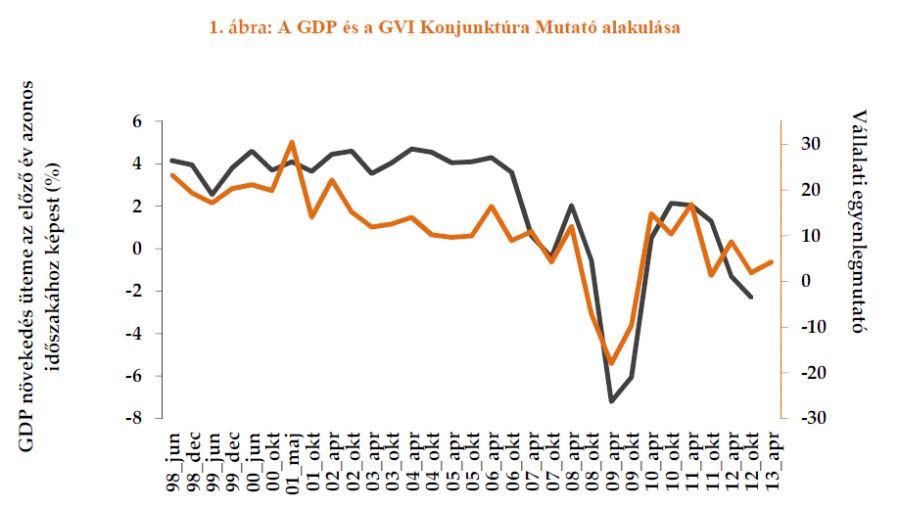

Read more >>>April 2013 was the thirty-first occasion of the HCCI Institute for Economic and Enterprise Research (IEER) business climate survey which is based on the cumulative response of more than 14,000 companies and conducted in April and October of each year, with the participation of regional chambers. It is the largest and most extensive business climate survey of its kind in Hungary. The research is part of the 14 million enterprise-wide Eurochambres survey of the European economy. In April this year 3,500 firms filled out our questionnaire -- our study is based on these responses.

The IEER business climate index rose 2.3 points from the October level of 1.9 points, and now stands at 4.2 points. This is still characterized as a weak positive result, which is underscored when the data is compared to the level in April of each year: this is the second lowest level since the start of the study (1998). The value of the uncertainty index is at the 43.6-point level. This suggests that within the business community there is still no clear or unanimous opinion of current trends. In addition, together with data available on the current performance of the Hungarian economy and the IEER business climate data, our attention is drawn to the slight decrease in uncertainty surrounding the current year.

Read more >>>The latest analysis from IEER looks at unreported income and explores their spatial variations using mathematical and statistical tools. This assessment measured sub-regional income and consumption data from 2010. The results estimate that unreported income represents 17.3% of total - both reported and unreported - income. The estimated unreported income was adjusted to a constant value so that at the national level the rate of unreported income is 18%.

In terms of regional differences it can be established that the proportion of income from the hidden economy is lower than average in high-income areas and those areas where the local economy and labour market are based on a few large companies. Most significant is the proportion of unreported income in areas where income corresponds to the regional average or slightly below. Another important finding is that only a quarter of small regions have an unreported income rate of less than 18%, whilst half of the country's population live in these areas.

April 2013 was the thirty-first occasion of the HCCI Institute for Economic and Enterprise Research (IEER) business climate survey which is based on the cumulative response of more than 14,000 companies and conducted in April and October of each year, with the participation of regional chambers. It is the largest and most extensive business climate survey of its kind in Hungary. The research is part of the 14 million enterprise-wide Eurochambres survey of the European economy. In April this year 3,500 firms filled out our questionnaire -- our study is based on these responses.

The IEER business climate index rose 2.3 points from the October level of 1.9 points, and now stands at 4.2 points. This is still characterized as a weak positive result, which is underscored when the data is compared to the level in April of each year: this is the second lowest level since the start of the study (1998). The value of the uncertainty index is at the 43.6-point level. This suggests that within the business community there is still no clear or unanimous opinion of current trends. In addition, together with data available on the current performance of the Hungarian economy and the IEER business climate data, our attention is drawn to the slight decrease in uncertainty surrounding the current year

On the following link an English summary of the paper can be downloaded.

Read more >>>January 2013 was the thirteenth occasion of the quarterly business climate survey of the Institute for Economic and Enterprise Research (IEER). For this study, a total of 400 companies are followed every quarter that are representative of the economic performance and sector distribution of firms operating in Hungary. A survey of changes in ten different business climate indicators related to the business situation and prospects of firms are analyzed and summarized in the format of the IEER Business Climate Index.

The latest results reveal a more favourable economic condition compared to the previous quarter. The IEER quarterly Business Climate Index increased significantly; following a low point from the previous quarter, it jumped to a level last measured in the second quarter of 2011. For both the current business situation of enterprises and short-term expectations positive changes uniformly took place in late 2012: in the following half-year all indicators had risen sharply. In terms of expected changes in staff numbers, optimism hitherto never before seen in the history of the survey was reported. After high growth in indicators for expected investment activity, those representing intensification of investments entered positive territory. The value for the uncertainty index compared to the previous quarter slightly decreased, indicating a decrease in the diversity of opinions on views toward the current and expected business situation of enterprises.

Read more >>>