- Research fields

- Further Research Areas

- Research year

- Related documents

The “Geography of Recession” research programme of the Institute for Economic and Enterprise Research (HCCI IEER), set the aim of analyzing the economic crisis from a regional point of view. Within this framework we provide detailed analyses on the changes of regional differences in the field of unemployment, layoffs and labour market quitting since the beginning of the economic crisis.

According to the latest figures, the amelioration that had started on the labour market in the first half year continued in the second half of 2010, although the degree of the improvement was very low. From May 2010 the registry showed relatively fewer job-seekers every month than in the previous year. On the basis of the survey of Hungarian Central Statistical Office it can be stated that though the number of employed increased and the number of unemployed decreased in the second half of 2010, these changes still do not mean a real breakthrough.

The regions of the north-western segment of the country having a more favourable economic position remained the winners of the upturn. In the micro-regions concentrating the export-oriented processing industry, the former downturn turned to a dynamic improvement. On the contrary, in the more backward southern and eastern regions the tendencies of unemployment have taken again an unfavourable turn in the winter months. Signs of any positive change are not discernible in the suburbia of the capital either: the number and the rate of job seekers is still increasing, though the rate does not even reach half of the national average. It seems that the capital’s labour market gives a belated response to cyclical fluctuations in the boom period as well.

Read more >>>

The Institute for Economic and Enterprise Research conducts a survey on the business climate among Hungarian enterprises since 1998. The survey relies on the answers of 1300-2000 managers and measures their opinion twice a year, every April and October and as such it gives the most extended sample of enterprises in Hungary among the similar business tendency surveys. Our research is part of an Eurochambres survey, all together involving more than 14 million enterprises to a European business tendency survey research program by now. In the past ten years, our findings seem to predict accurately the expected change in the GDP of Hungary. Our key findings had been used by OECD, IMF and the Hungarian government as well.

This time, our database consists the answers of 1803 enterprises. After the turning-point in October 2009, the business anticipations of Hungarian enterprises are continuously ameliorated: the indicators seem still to be in positive range even in comparison with last year. While the IEER Business Climate Index stayed at +10.4 last October, by April 2011 it reached +16.8. According to our results, the recession in the Hungarian economy is now over its nadir, there are improving business anticipations and business confidence. Although way out of recession has started in October 2009, the process is rather slow.

The IEER Uncertainty Index did not change over the last half a year; still stays at value 45.5 which is considered to be high. This means that there are still a significant number of enterprises without counting on the improvement of business climate.

Read more >>>

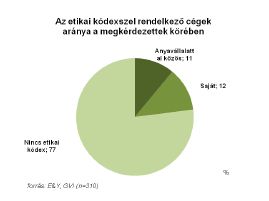

According to a recent study – made in the co-operation of Ernst & Young and the Institute for Economic and Enterprise Research –, 30 % of the Hungarian top managers would not reject a bribe offer. This is only one statement from the research which studied the attitudes of top managers toward corruption and the institutional corruption risks.

Read more >>>

The research concentrated on outlining suggestions for the Kecskemét Regional Integrated Vocational Training Centre not-for-profit organization (KETISZK) in two, closely related topics: business strategy improvement and monitoring system. Our study on business strategy gives an overview on the current situation of KETISZK and outlines four consecutive strategical scenarios. Internal and external factors will be reviewed such as the general model of Regional Integrated Vocational Training Centre, the specific characteristics of KETISZK, general demographic trends in the expected number vocational school students, trends in labour market, regulatory issues, and the effects of the intended investment of Daimler-Benz AG. Four strategical scenarios can be derived from the analysis of the current situation, in the following logical order:

The four scenarios are as follows:

-

Sustainable KETISZK

-

KETISZK as information center

-

KETISZK in coordinating role

-

KETISZK as center of innovation

The study also aims to introduce an effective monitoring system which helps to analyse the professional career paths of graduated students with significance to the situation of recent vocational students. Due to the monitoring system, now we can get a general picture on how the KETISZK graduated students accomplish labour market expectations, and what are their typical career paths further on.

Our intention was to outline scenarios and suggest alterations that consider not only the aims of KETISZK but also the scant opportunities. As a result, the study considers a (1) synergic, (2) open, (3) easy to use, and (4) extensible database a viable option.

Read more >>>

The Institute for Economic and Enterprise Research - in collaboration with the Hungarian Ministry for National Economy - conducted a research on the expected demand of labour and short-term business expectations of 7550 enterprises this year.

Results show recession made a strong negative mark on the labour market during 2009. The turning-point in economic growth did not mean a turning-point in the labour market: employment rates continuously dropped during 2009 and there was only a slight increase in Q2 2010. Indicators show that business climate and anticipations of enterprises are continuously increasing since the second half of 2009 and by now they reached their pre-recession value. However, the tendency that anticipations for the near future are deteriorating reveals that the positive tendencies are very fragile and the way out of the recession might take a long time.

The results of our labour market prognosis show that anticipations of enterprises are more sanguine than last year. Export-oriented, wholly foreign-owned enterprises in the service industry are the most optimistic. The demand for labour of skilled workers and graduated professionals has increased compared to last year and a continuous demand can be anticipated for the next year as well.

Read more >>>

According to the latest estimates from IEER, the macroeconomic situation of the SMEs was more favorable in Q3 2010: there was a 1.6% increase in the GDP compared to the same period previous year and a 0.8% increase compared to the previous quarter (Q2 2010).

Latest dataset of HCCI IEER (from October 2010) on SMEs indicates that the conjuncture indicator followed the positive changes prevalent in the macroeconomic conditions. There was similar levels of increase in the values of all – either former or present – conjuncture indices in Q3 2010.

The positive perceptions on the present situation, however, do not contribute to positive short-term expectations: the values of all the indicatiors deteriorated during the last three months except the perceptions on profitability that stagnated and the pre planned rate of investment activity that actually grew.

Overall, the SME Conjuncture Index has shown slightly increasing tendencies in Q3 2010, and reached its peak value since July 2008. However, there has been an increase in the dispersion of SMEs' opinions on the future expectations comparing to the previous quarter (Q2), which implies the tendency of growing heterogenity in the future expectations of SMEs' throughout 2010.

Read more >>>

The survey on the perspective of enterprises about the recession had been repeated for the third time by the Institute for Economic and Enterprise Research.We provide analysis not only on the general characteristics of enterprises and different indicators of conjecture, but also on borrowings, foreign currency risks and financial disciplines of enterprises and the preventive actions they took in order to avoid the negative effects of the recession. Moreover, we had interest in mapping the internet usage habits at Hungarian enterprises. The three datasets are available free of charge at the following web addresshttp://www.ola.gvi.hu/.

The results of the analysis revealed that the Hungarian enterprises did not change their developed techniques and actions in order to avoid the negative effects of the recession. Companies with foreign ownership share and export-oriented companies are usually very adaptive to the new conditions than other companies. Also, there is a strong correlation between the business situation and the adaptation skills: the worse the business situation of an enterprise the broader the range of techniques it adapts to avoid the worst case scenario.

The analysis also reveals that one part of the enterprises were so extensively affected by the recession that they were technically forced to find every possible way to reduce the negative effects. Favorable business situation thereby facilitates long-term strategic planning and action, while bad business situation makes short-term downsizing and production restraint more probable. We also tried to prove our surmise that those companies who use internet actively will be more likely to have a faster recovery from the recession but this hypotheses could not be fully tested and measured by solely relying on data about the business situation of enterprises.

The findings based on the three datasets were presented in English at CIRET Conference, Economic Tendency Surveys and the Services Sector on the 14thOctober 2010. See also (https://www.ciret.org/conferences/newyork_2010).The analysis, the power point slides and the survey of the research (from March and June) can be found and downloaded in the appendix.

Read more >>>

This is the 26th time that the Institute for Economic and Enterprise Research conducts a survey on the business climate among Hungarian enterprises. The survey relies on the answers of 1300-2000 managers and measures their opinion twice a year, every April and October and as such it gives the most extended sample of enterprises in Hungary among the similar business tendency surveys. Our research is part of an Eurochambres survey involving 14 million enterprises.

This time, our database consists the answers of 1869 managers. After the turning-point last October, the anticipations of Hungarian enterprises are continuously ameliorated by April and by October as well: the indicators seem still to be in positive range. However, if we compare our latest results with the findings from April 2010, there can detect only moderated positive tendencies in the anticipations for the near future. While the IEER Business Climate Index stayed at -9% last October, and in April it reached its peak at +14.8%, by October it dropped again and now stays at 10.4%.

Read more >>>

The research program "Vocational schools" by IEER conducted since 2008 includes two main parts. The aim of the company survey is to map the demand of specific segments in the business sector for vocational school graduates within one year and beyond a three-year time span.

The survey on graduates examines the beginning of the working life of those young people who obtained their qualifications in vocational schools or trade schools 19 months before. The research has a focus point on whether these young people were able or willing to enter the labour market during the 19 months after their graduation.

Read more >>>

According to the latest estimates, there was a set-back in the continuous amelioration of GDP in Q2 2010 that might have gotten prolonged the way of the Hungarian economy out of the recession. This temporary stagnation does not affect the different sectors in economy though: the total value both consists favorable values from the trade sector and gruesome data from the building industry.

The SME Conjuncture Index has shown only slightly increasing tendencies in Q2 2010 - its value in July is 0,0231 while in April it was 0.0251, whereas the value of Business Uncertainty Index has significantly increased by 0.41. Our results also report on a more and more frequently appearing phenomenon, the chain indebtedness: more than half of our respondents acknowledged that late payments affected them in the last 6 months. Our data set from June 2010 also reveals the fact, that small and medium enterprises estimate the interval for 13 month they would need for a complete recovery from the economic recession.

Read more >>>